Market Intelligence Newsletter

By Marlon Schwarcz · 2026-06-26

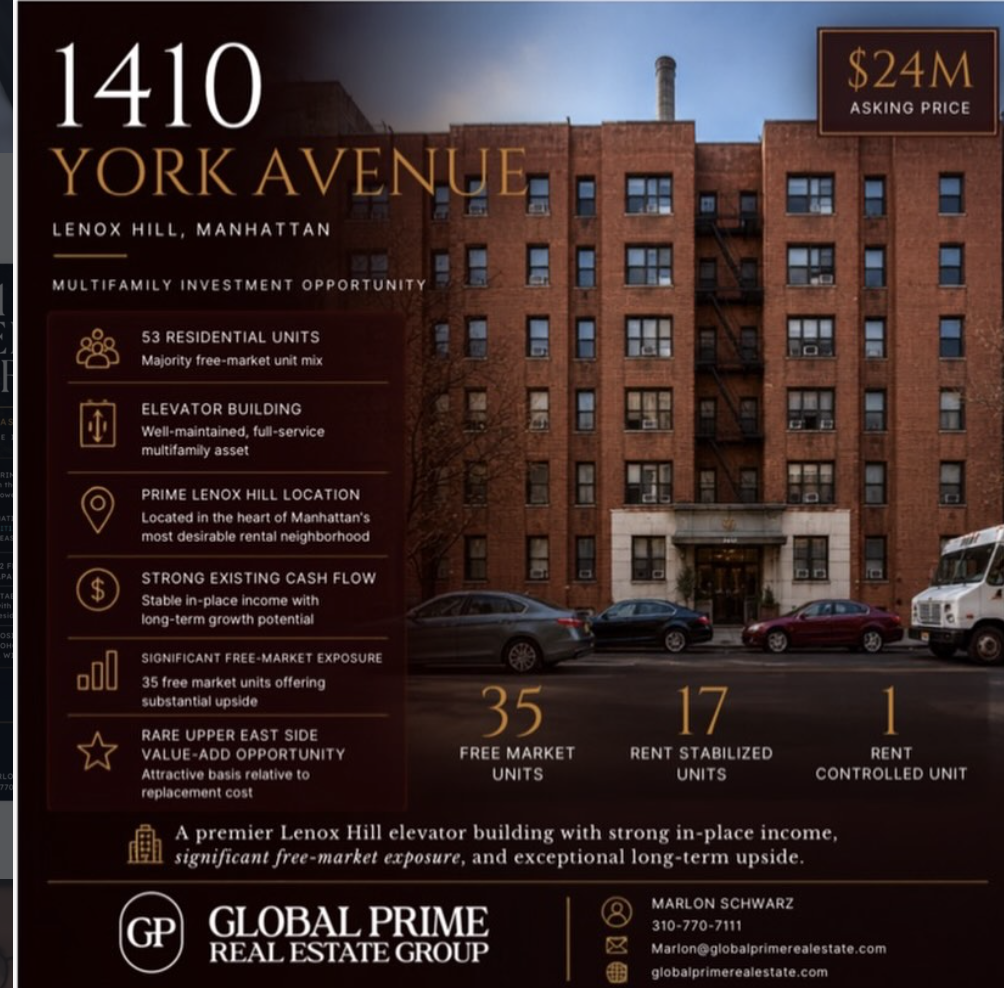

Featured Listing: 1410 York Avenue, Lenox Hill, Manhattan

Asking Price: $24,000,000

There are multifamily assets in Manhattan that function as conventional income-producing properties, and then there are assets that behave more like long-duration income instruments embedded within irreplaceable urban land. 1410 York Avenue belongs to the latter category.

The property is a 53-unit, full-service elevator multifamily building located in Lenox Hill on the Upper East Side. It sits within one of Manhattan’s most established and structurally supply-constrained residential submarkets, where rental performance is shaped by long-term demand drivers rather than short-term economic cycles.

This is not a redevelopment opportunity. It is not a turnaround situation. It is a stabilized income-producing asset with embedded rent growth potential driven primarily by lease turnover and gradual market convergence over time.

Lenox Hill continues to rank among the most resilient rental markets in New York City. Demand is supported by proximity to major hospital systems, Midtown East employment corridors, and the broader Upper East Side residential ecosystem.

Tenancy in this submarket tends to be longer in duration, with consistently strong absorption and short vacancy periods. This creates a rental environment defined by stability and durability across market cycles rather than volatility.

Within this context, 1410 York Avenue presents a differentiated rent structure. The building consists of 53 residential units, with approximately 35 units operating on a free-market basis.

This level of deregulated exposure is increasingly rare in comparable Upper East Side multifamily assets, where rent stabilization often limits near-term income movement.

The free-market component is the primary driver of the investment thesis, creating a direct relationship between lease turnover and income growth as rents gradually converge toward prevailing market levels in Lenox Hill without requiring redevelopment or capital-intensive repositioning.

The remaining units consist of approximately 17 rent-stabilized apartments and 1 rent-controlled unit. These stabilized components provide predictable baseline cash flow and reduce income volatility across market cycles. At the same time, they introduce a staggered transition profile in which portions of the rent roll gradually shift toward higher income potential over an extended time horizon.

This structure results in a layered income profile rather than a single-step value event, supporting incremental realization of upside over time.

From a market structure standpoint, Manhattan multifamily continues to be defined by constrained new supply and rising replacement costs. New development in the Upper East Side remains limited due to zoning restrictions, entitlement complexity, and elevated construction economics.

At the same time, the cost to replicate existing housing stock continues to increase, reinforcing a structural valuation fl